A Multi-Million Dollar Campaign Built on a Half-Truth

If you’ve spent any time on the internet researching retirement planning, you’ve almost certainly encountered Fisher Investments’ aggressive advertising campaign against annuities. Their ads carry headlines like “Why I Hate Annuities,” and their marketing materials — including their widely distributed “Annuity Insights” guide — paint annuities as complex, fee-laden traps designed to confuse retirees and enrich insurance companies.

It’s compelling marketing. It’s also deeply misleading.

Here’s the central problem: Fisher Investments is almost exclusively attacking variable annuities — a specific, securities-based product that is fundamentally different from fixed annuities and fixed indexed annuities. Yet their advertising rarely makes this distinction clear to the average consumer. The result is that millions of Americans who could genuinely benefit from the safety and guarantees of a fixed or indexed annuity are being steered away from products they never even knew existed — and toward Fisher Investments’ fee-based portfolio management instead.

Let’s examine exactly what Fisher gets wrong, why they get it wrong, and what the factual truth about fixed and indexed annuities actually is.

The Sleight of Hand: Conflating Three Very Different Products

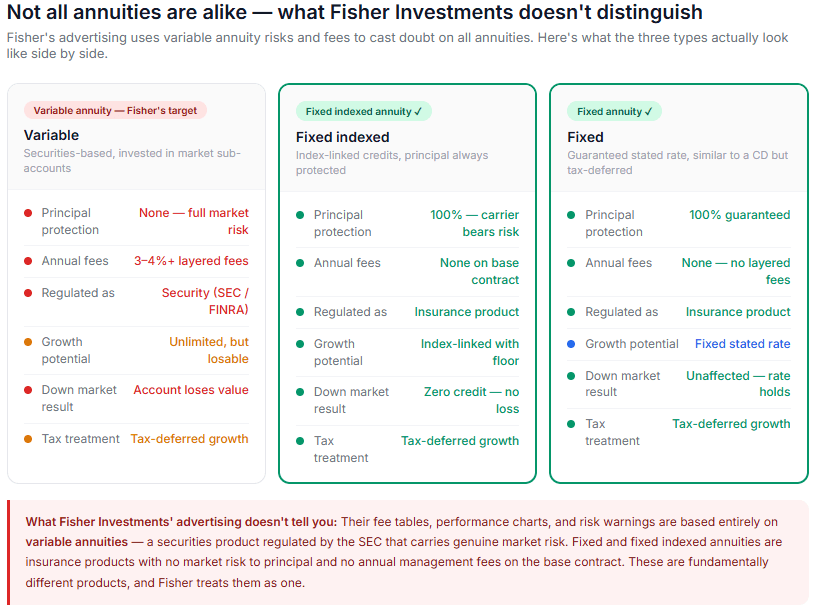

To understand Fisher’s misleading approach, you first need to understand that “annuity” is a broad category — not a single product. There are three primary types:

1. Variable Annuities Variable annuities are insurance contracts that allow the owner to invest premiums in market-based sub-accounts, similar to mutual funds. Their value fluctuates with the market. They carry investment risk, can lose value, and often come with the high layered fees Fisher describes — mortality and expense fees, subaccount fees, rider fees — that can stack up to 3.5% or more annually.

Fisher’s criticism of variable annuities? Much of it is valid.

Variable annuities are complex securities products. They are regulated by the SEC and FINRA, require a securities license to sell, and carry genuine market risk. The fee structures can be burdensome. They are not appropriate for every investor, and they have historically been oversold to consumers who didn’t fully understand them.

2. Fixed Annuities Fixed annuities are straightforward insurance contracts that guarantee a fixed rate of return over a specified period — similar in structure to a bank Certificate of Deposit, but typically with more favorable rates and tax-deferred growth. They are not securities. They carry no market risk. The insurance company bears all investment risk, and the contract owner is guaranteed their principal plus a stated rate of interest.

3. Fixed Indexed Annuities (FIAs) Fixed indexed annuities offer interest credits linked to the performance of a market index — such as the S&P 500 — but with a crucial protection: the contract owner’s principal is never directly exposed to market losses. When the index goes up, the owner receives a credit (subject to caps or participation rates). When the index goes down, the owner receives zero — not a loss, zero. Their principal remains intact.

Fisher Investments’ “Annuity Insights” guide references all three types on page two — and then spends the remaining pages almost entirely attacking the costs and risks of variable annuities, while the charts, fee tables, and performance comparisons are built exclusively around variable annuity data. A reader who doesn’t already know the difference — which is most consumers — will walk away believing all annuities carry the same risks, fees, and drawbacks. They do not.

Dissecting Fisher’s “Annuity Insights” Guide: Claim by Claim

The Fee Argument

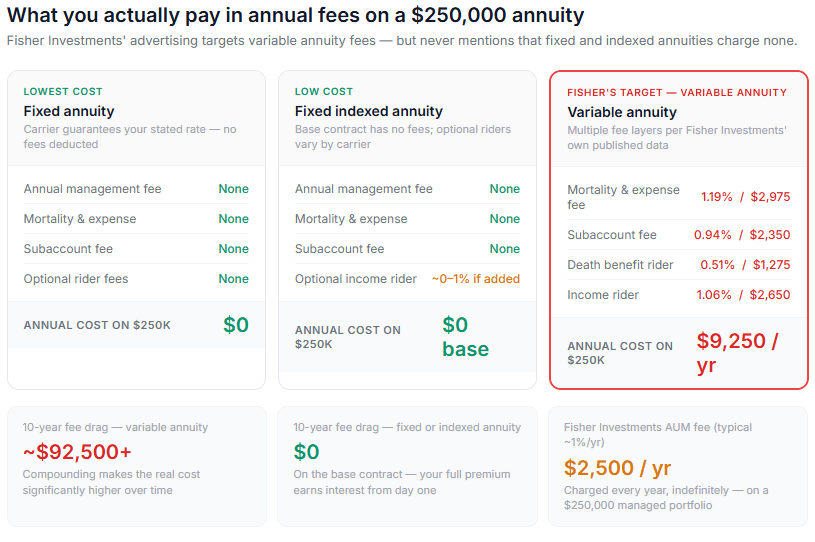

Fisher’s guide presents a fee table showing a hypothetical variable annuity with a total annual cost of 3.70%, broken down as:

- Mortality & Expense Fee: 1.19%

- Subaccount Fee: 0.94%

- Death Benefit Rider: 0.51%

- Income Rider: 1.06%

They then show a compelling chart demonstrating how a $100,000 investment grows to $836,596 in a blended index, but only $302,158 after variable annuity expenses over roughly 27 years. It’s a powerful illustration.

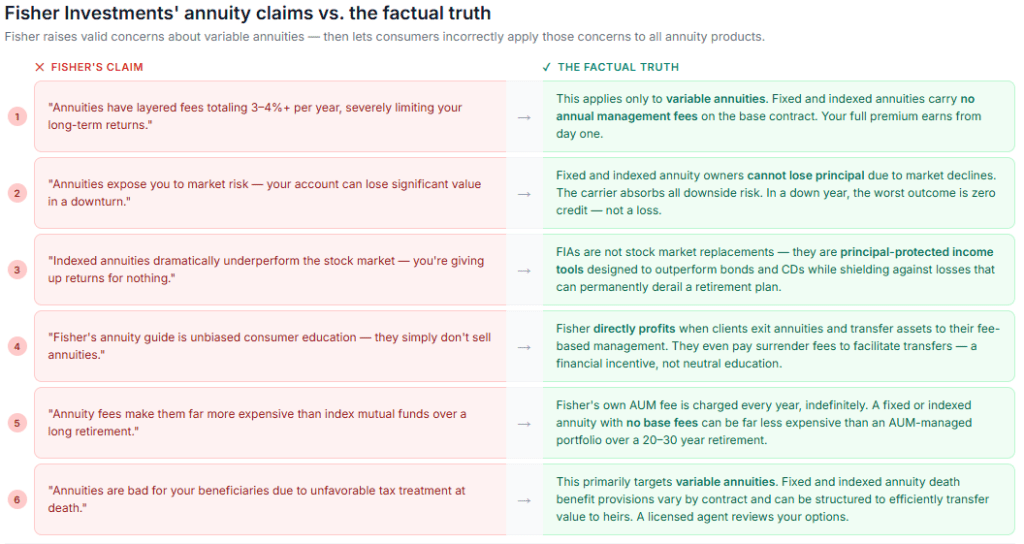

What they don’t tell you: Fixed annuities and fixed indexed annuities have no annual management fees in most cases. There are no subaccount fees because there are no subaccounts. There are no mortality and expense charges structured the same way. Optional riders on indexed annuities may carry fees, but the base product does not. The fee comparison Fisher uses is entirely inapplicable to the products that make up the majority of annuity sales in the United States today.

According to LIMRA, fixed indexed annuities have consistently outsold variable annuities in recent years, representing the largest segment of annuity sales. Fisher’s guide attacks the fee structure of the smaller and declining segment of the market while ignoring the product most Americans are actually buying.

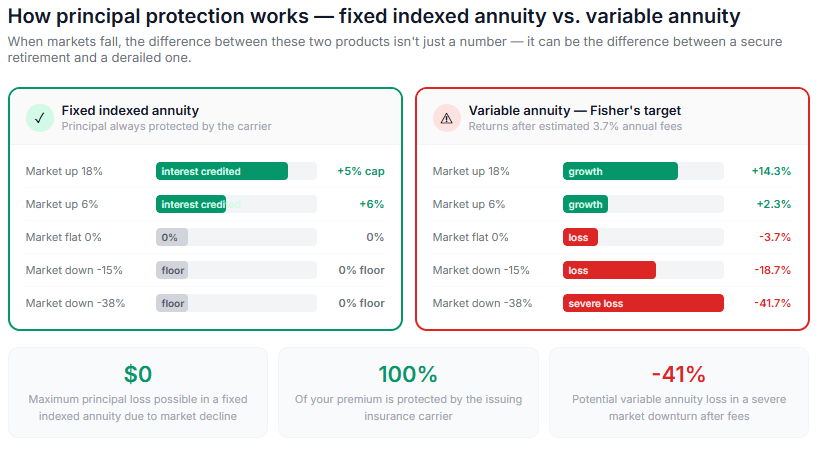

The Performance “Floors and Caps” Argument

Fisher’s guide dedicates significant space to showing how indexed annuity caps limit long-term growth. Their hypothetical example uses a 1% floor and a 5% annual cap, and shows that over 27 years, this hypothetical product dramatically underperforms the S&P 500.

What they don’t tell you — and this matters:

First, the comparison is intellectually dishonest. No financial professional with integrity would tell a client that a fixed indexed annuity is a replacement for direct equity investment. They are fundamentally different tools for different purposes — one provides market-linked growth potential with principal protection, the other provides full market participation with full market risk. Comparing them directly is like arguing that a seatbelt is a poor substitute for not getting into a car accident.

Second, Fisher’s hypothetical caps are cherry-picked to produce a dramatic result. Current FIA products from highly-rated carriers offer a variety of crediting strategies — annual point-to-point, monthly sum, volatility-controlled indexes, and others — with varying cap and participation rate structures. Many indexed annuities today also offer uncapped strategies with participation rates that can deliver meaningful index-linked growth.

Third — and most critically — Fisher’s chart does not account for the years the S&P 500 lost money. The 2000-2002 dot-com crash. The 2008-2009 financial crisis. The 2022 bear market. In each of those periods, a fixed indexed annuity owner lost nothing. An investor in Fisher’s recommended blended portfolio lost a significant portion of their account value. For a retiree in or near the distribution phase of their life, those losses are not just numbers on a statement — they can permanently impair a retirement income plan.

The Inflation Argument

Fisher correctly notes that annuity income is typically not adjusted for inflation, and illustrates a hypothetical 10-year shortfall of $88,454 based on 3% annual inflation against a flat $50,000 annuity payment.

This is a legitimate consideration — and one that any competent insurance agent discusses with clients. However, it applies equally to any fixed-income strategy, including bonds and CDs. Fisher doesn’t apply the same inflation critique to bond portfolios. More importantly, this argument misrepresents how annuities are typically used in a comprehensive retirement plan.

Most financial planners and insurance professionals do not recommend placing a client’s entire retirement savings into an annuity. Fixed and indexed annuities are commonly positioned to cover baseline, non-discretionary expenses — housing, food, healthcare premiums — while other assets remain invested for growth. The annuity provides a guaranteed floor of income the client cannot outlive, not a complete retirement solution. That is their purpose, and they fulfill it exceptionally well.

The Tax Argument

Fisher’s guide notes that annuity withdrawals are taxed as ordinary income rather than at capital gains rates, and that holding an annuity inside a traditional IRA provides no additional tax advantage.

These are accurate statements. They are also, in context, incomplete.

The tax-deferred accumulation within an annuity held in a non-qualified (taxable) account can be a meaningful advantage for clients in higher income years who expect lower income in retirement. Additionally, the tax treatment of annuity income in certain structured payout scenarios — particularly immediate annuities with an exclusion ratio — can result in a portion of each payment being received income-tax-free as a return of principal.

The IRA point is valid, and it’s a good consumer education point. It is not, however, an argument against annuities broadly — it’s an argument for proper placement of annuities in the right account type. A licensed insurance professional helps clients make exactly these determinations.

The Beneficiary / Step-Up in Basis Argument

Fisher notes that most variable annuities do not receive a step-up in cost basis at death, creating a potentially larger income tax burden for beneficiaries compared to other inherited investments.

This is accurate for variable annuities. Fixed and indexed annuities have their own death benefit structures that vary by contract, and this is always a factor to review with both an insurance professional and a tax advisor. It is not a universal indictment of all annuity products.

The Conflict of Interest Fisher Doesn’t Disclose in Its Advertising

Here is the question every consumer should ask when reading Fisher Investments’ anti-annuity materials: Who benefits when you don’t buy an annuity?

Fisher Investments is a registered investment adviser that manages client portfolios for a fee typically based on assets under management (AUM). When a client holds an annuity, those assets are generally not available for Fisher to manage. When a client surrenders an annuity and transfers the proceeds to Fisher, Fisher earns a management fee on those assets — every year, indefinitely, for as long as the client remains with them.

Fisher’s own “Annuity Insights” guide concludes with an offer to compensate clients for “some or all of the annuity surrender fees incurred when liquidating your annuity” — provided the proceeds are transferred to Fisher for management. Read that again: Fisher Investments will pay your surrender fees if you give them your money to manage.

That is not consumer education. That is a direct financial incentive to move assets under Fisher’s management, dressed up as altruistic guidance. The guide states on its first page that “we do not sell annuities — our aim is to provide you an insightful view of these products.” What it does not say with equal clarity is that Fisher profits directly when consumers act on this “insightful view” and transfer their assets to Fisher.

Fixed and indexed annuity agents earn a one-time commission paid by the insurance carrier. There is no ongoing annual fee deducted from the client’s account. The client’s full premium goes to work for them from day one. Fisher’s AUM-based model, by contrast, deducts a percentage of assets every single year — a fee structure that, over a 20 or 30-year retirement, can represent a very significant cost.

What Fixed and Indexed Annuities Actually Offer

Let’s be clear about what these products genuinely provide — and what they don’t.

What they offer:

- Principal protection. In a fixed or indexed annuity, the insurance carrier — not the client — bears market risk. A client who places $200,000 into a fixed indexed annuity will never receive a statement showing $150,000 due to a market decline.

- Guaranteed minimum interest. Fixed annuities guarantee a stated rate. Indexed annuities guarantee a minimum — typically 0% or a small positive floor — so that in down market years, the client’s account does not decrease.

- Tax-deferred accumulation. Interest credited inside an annuity is not taxable until withdrawn, allowing for compound growth without annual tax drag in non-qualified accounts.

- Guaranteed lifetime income options. Riders or annuitization options can provide income the client cannot outlive, regardless of how long they live or what markets do — a feature no portfolio of stocks and bonds can replicate with certainty.

- Carrier-backed guarantees. Annuity guarantees are backed by the financial strength of the issuing insurance company, and in most states are further protected by state guaranty associations up to specified limits.

- Liquidity provisions. Most fixed and indexed annuities allow penalty-free withdrawals of 10% of the account value annually, and many include waivers for confinement in a nursing facility or terminal illness diagnosis.

What they are not:

- They are not designed to maximize long-term equity-market returns. A client with a 30-year time horizon and high risk tolerance may be better served by other investment strategies.

- They are not completely without restrictions. Surrender periods are real, and clients must understand and accept the liquidity limitations before purchasing.

- They are not appropriate for 100% of a client’s assets in most cases. They are tools, best used as part of a comprehensive plan.

The Bottom Line: Consumers Deserve Accurate Information

Fisher Investments spends heavily — by some estimates millions of dollars per month — on advertising that creates fear and confusion about annuities in the minds of American retirement savers. Their materials are carefully constructed to be technically defensible while being practically misleading, because they focus almost entirely on variable annuities while using language and framing that causes consumers to apply those criticisms to all annuity products.

The result is that real people — people who would genuinely benefit from the security, the guarantees, and the peace of mind that a properly structured fixed or indexed annuity can provide — are being frightened away from a tool that could meaningfully improve their retirement security.

Fixed and indexed annuities are not perfect for everyone. No financial product is. But they are legitimate, regulated, carrier-backed products that have provided millions of Americans with exactly what they need most in retirement: certainty.

Certainty that their principal is protected. Certainty that they will have income they cannot outlive. Certainty that a bad year in the stock market will not derail their retirement plan.

Before making any decision about annuities — or about moving assets away from an annuity — consumers deserve to hear the complete story. Not just the version that benefits the firm telling it.